The past year has been characterised by strong contrasts and disparate regional dynamics. In this market, the .fr domain has once again performed well.

Afnic, the association responsible for several Internet TLDs including the .fr domain, shares its annual analysis of the global domain name market. In this new opus, the association deciphers global trends and highlights the specific characteristics of the different segments and the regional particularities.

Key figures

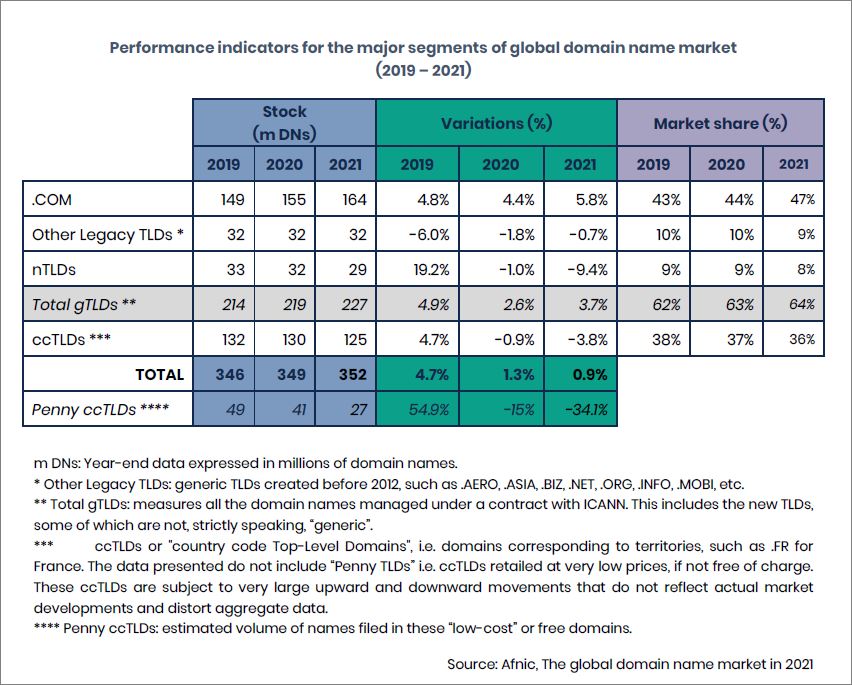

The global domain name market accounted for approximately 352 million domain names at the end of December 2021, up 0.9% compared to the 1.3% in 2020.

Although the growth trend shows a constant slowdown (+4.7% in 2019, +1.3% in 2020, +0.9% in 2021), an analysis of monthly variations reveals that in reality, 2021 was the “trough” year and that the market was once again on an upward trend at the end of year.

Breakdown:

- 164 million .com and 32 million “other Legacy TLD”(.net, .org, .biz, etc.);

- 125 million ccTLDs (so-called “country” TLDs, corresponding to a territory or country like the .fr domain);

- 29 million “new TLDs” created from 2014 onwards (nTLDs encompass different segments including the geoTLD – .bzh, .paris, .alsace, .corsica, etc. – TLDs corresponding to brands – .sncf, .mma – community TLDs and generic TLDs).

.com: a leader whose dynamic is under threat

The .com domain dominates the market not only in terms of volume (accounting for 84% of all Legacy TLDs) but also in terms of growth due to rising numbers of create operations and a stable retention rate. In 2021 it posted a market share of 47% and +5.8% growth compared with 2020 (against +4.4% in 2019).

This recovery is partly explained by the resumption of domaining activities following the slowdown caused by COVID.

This domain is one to watch though next year as its price underwent a 7% increase on 1 September 2021, with a further 7% increase scheduled for 1 September 2022.

“Country” ccTLDs: often leaders in their region

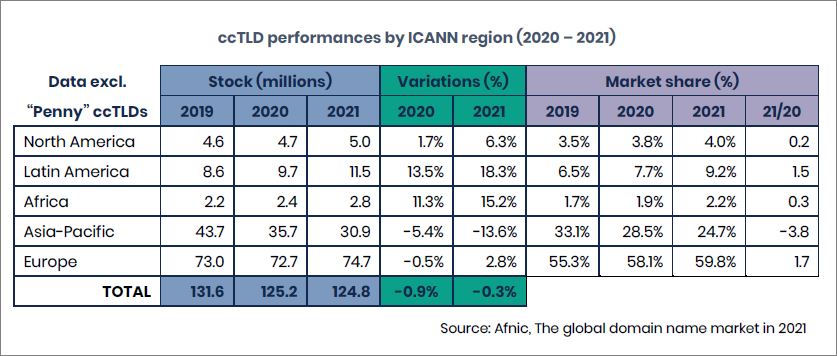

“Country” TLDs (ccTLDs) represent the second largest segment after the .com domain. They posted a slight decline in market share of -1% and a stock loss of 3.8%. ccTLDs still remain the leaders in most regions: 63% in Africa, 69% in Latin America, 46% in Asia-Pacific (compared to 37% for the .com domain), 62% in Europe. With the noteworthy exception of North America where the .com domain has taken root and flourished (76% of market share).

As the table below shows, the development of ccTLDs shows strong disparities between regions:

- two regions are closing the “gap”: Latin America and the Caribbean recorded the highest growth rate (+18.3%) followed by Africa (+15.2%).

- North America recorded 6.3% growth and Europe 2.8%;

- Asia-Pacific, meanwhile, recorded a 13.6% fall in stock, primarily due to the .CN (China) and .TW (Taiwan) domains.

Europe remains the region where ccTLDs thrive best: out of 31 ccTLDs with over a million names, 18 are in Europe, compared with 7 in Asia-Pacific, 3 in Latin America and the Caribbean, 2 in North America, and 1 in Africa. It is also interesting to note that in Europe, the .fr domain recorded the highest growth at +5.8%.

New TLDs: considerable market variations caused by a small number of domains

nTLDs posted stock losses of -9% (vs. -1% in 2020 and growth of +19% in 2019), with a market share of 8%.

Created in 2014 to give greater choice by offering more expressive alternatives, nTLDs represent the minority segment. The segment is for the most part sustained by several leading domains, given that 62% of nTLDs (excluding .BRAND) have fewer than 10,000 names in their portfolio. The global stock loss in 2021 is the result of the significant decline of leaders like .ICU (-88%).

Concentration of market players

An analysis of market shares, whether at the level of domains, registrars or back-end operators, reveals that the domain name sector is divided between a handful of major players accounting for the majority of market shares and a spattering of small players.

Of the top ten world registrars, six are American, one Chinese, one Indian, one German and one Japanese. The ranking within the TOP 10 has changed but its composition remains the same.

The other major determinant of the market is location, the most powerful registrars being located in North America (50% of registrars managing more than 1 million domain names). Their counterparts in other regions are smaller, and sell ccTLDs just as well as, if not better than, gTLDs and nTLDs in order to respond to local demand and to the competition to which it leads.

Download the full Study

About Afnic

Afnic is the acronym for Association Française pour le Nommage Internet en Coopération, the French Network Information Centre. The registry has been appointed by the French government to manage domain names under the .fr Top Level Domain. Afnic also manages the .re (Reunion Island), .pm (Saint-Pierre and Miquelon), .tf (French Southern and Antarctic Territories), .wf (Wallis and Futuna) and .yt (Mayotte) French Overseas TLDs.

In addition to managing French TLDs, Afnic’s role is part of a wider public interest mission, which is to contribute on a daily basis, thanks to the efforts of its teams and its members, to a secure and stable internet, open to innovation and in which the French internet community plays a leading role. As part of that mission, Afnic, a non-profit organization, has committed to devoting 11% of its Revenues from managing .fr Top Level Domain to actions of general interest, in particular by transferring €1.3 million each year to the Afnic Foundation for Digital Solidarity.

Afnic is also the back-end registry for the companies as well as local and regional authorities that have chosen to have their own TLD, such as .paris, .bzh, .alsace, .corsica, .mma, .ovh, .leclerc and .sncf.

Established in 1997 and based in Saint-Quentin-en-Yvelines, Afnic currently has nearly 90 employees.

On the same topic

Featured

News

07/20/26

Afnic named registry for eight French overseas TLDs

Afnic, the association responsible for .fr and several French ...

Expert papers

How can the DNS help identify drones remotely?

As part of the Télécom SudParis Cassiopée programme, Afnic ...

Agenda

10/17/2026